Union Budget 2026 - Income Tax in India - Key Highlights

The Union Budget 2026 introduces major reforms aimed at improving ease of business, lowering compliance burden, rationalizing penalties, improve taxpayer relief, and promoting manufacturing, MSMEs, IFSC entities, and technology sectors. Understanding these changes is essential for accurate tax filing, better planning, and financial optimization.

1. Extended Due Date for Filing Income Tax Returns

Section 139(1)

New Due Dates

| Category | Earlier | New |

|---|---|---|

| Individuals (ITR 1 & ITR 2) | 31 July | Unchanged |

| Individuals (Non-Audit) & Trust | 31 July | 31 August |

| Businesses (Audit) | 31 October | Unchanged |

2. Revised Return Filing — More Time Granted

Section 139(5)

Old Rule

Revised return allowed only till 31 December

New Rule (Budget 2026)

Revised return allowed up to 31 March of the Assessment Year

- Example: FY 2025-26 return can be revised till 31 March 2027

3. Updated Return (ITR-U) — Relaxed Conditions

Section 139(8A)

Earlier Restrictions

Not allowed if:

- Loss reduced

- Refund claimed

- Notice issued

Now Allowed Even If

- Loss is reduced

- Refund claim changes

- Notice under reassessment issued

Additional Tax

| Time of Filing | Additional Tax |

|---|---|

| Within 12 months | 25% |

| Within 24 months | 50% |

| Within 36 Months | 60% |

| Within 48 Months | 70% |

| If After notice u/s 280 | +10% of Aggregate Tax & Interest |

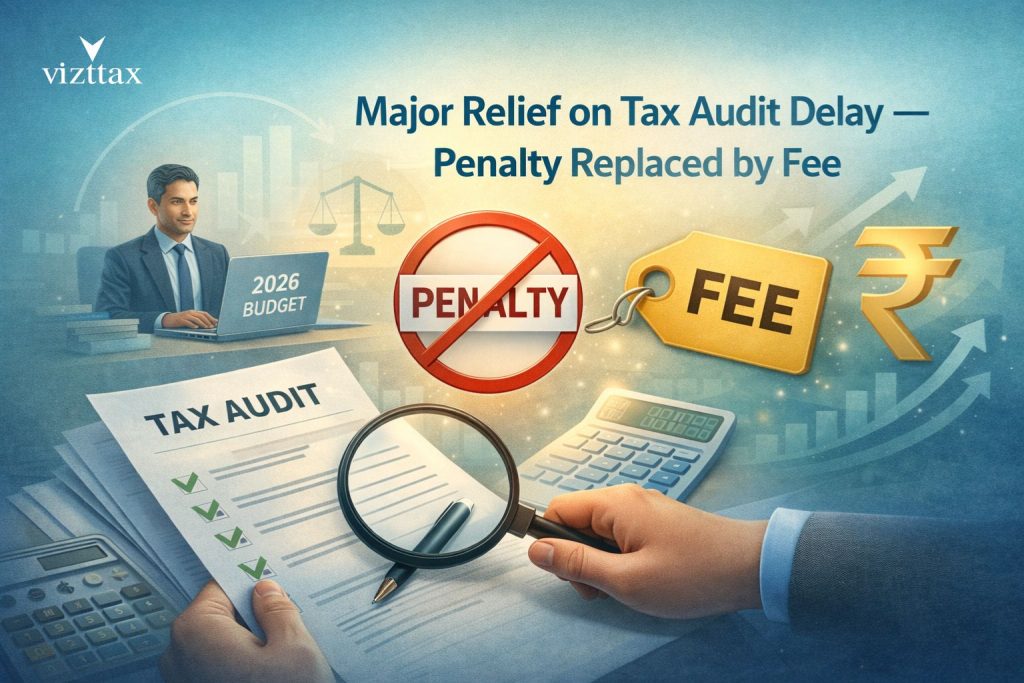

4. Major Relief on Tax Audit Delay — Penalty Replaced by Fee

Section 44AB & Section 271B (Amended)

Earlier Rule

- Penalty: 0.5% of turnover

- Maximum penalty: ₹1,50,000

New Rule (Effective FY 2026-27)

- Penalty abolished

- Fixed late-filing fee introduced instead

- Fee will depend on delay period

- No criminal exposure for technical delay

| Timeline | Late Fee |

|---|---|

| Delay up to One month | ₹75,000 |

| Delay beyond One Month | ₹1,50,000 |

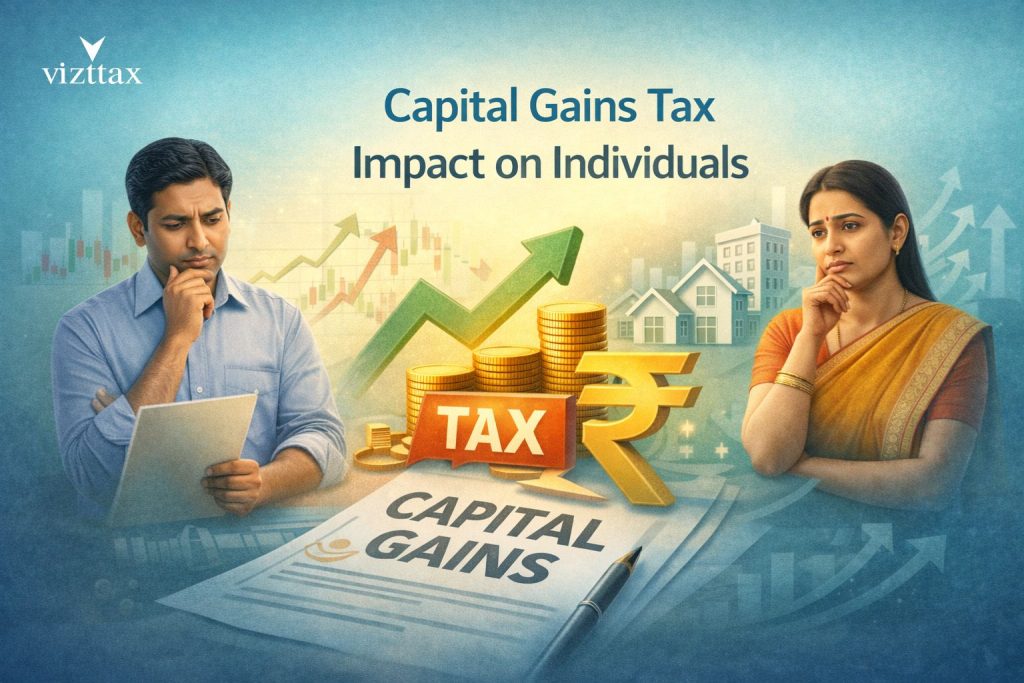

5. Capital Gains Tax Impact on Individuals

Section 111A, 112, 115QA

Buy-Back of Shares

Buy-back income now taxed as capital gains, not dividend

Promoter tax:

- Domestic Corporate promoters: 22%

- Other individuals: 30%

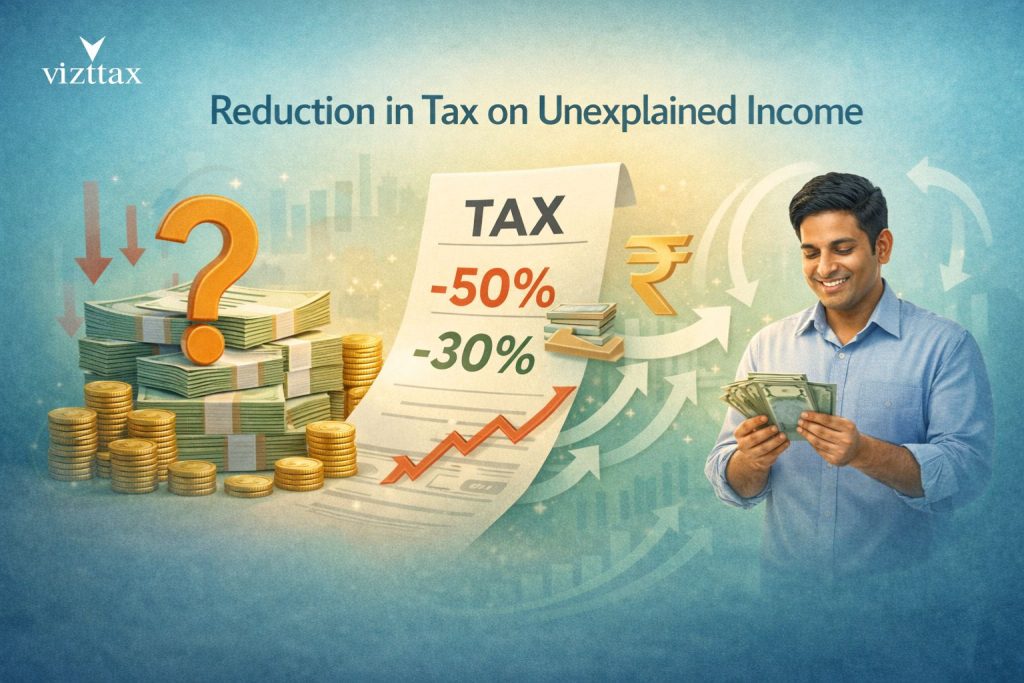

6. Reduction in Tax on Unexplained Income

Section 68, 69, 115BBE

| Earlier | Now | |

|---|---|---|

| Tax Rate | 60% | 30% |

| Penalty | 10% | Omitted |

7. TDS & TCS Changes Affecting Individuals

Section 194C, 194Q, 206C

TDS Changes

- Manpower supply treated as contract work

- Motor Accident Tribunal interest TDS exempt

TCS Rate Updates

| Transaction | Old Rate | New Rate |

|---|---|---|

| Overseas Tour | 5% & 20% | 2% |

| Education / Medical LRS | 5% | 2% |

| Scrap Sale | 1% | 2% |

| Sale of minerals, being coal or lignite or iron ore | 1% | 2% |

| Alcohol Liquor for Human Consumption | 1% | 2% |

| Tendu Leaves | 5% | 2% |

8. Securities Transaction Tax (STT) Increase

Chapter VII

| Instrument | Old STT | New STT |

|---|---|---|

| Futures | 0.02% | 0.05% |

| Options | 0.1% | 0.15% |

9. Minimum Alternate Tax (MAT) Reforms

Section 115JB

Major Changes

| Particular | Earlier | Budget 2026 |

|---|---|---|

| MAT Rate | 15% | 14% |

| MAT Credit | Allowed | Final tax; no new credit |

| MAT on Non-Residents | Applicable | Not applicable in presumptive cases |

10. Corporate Tax Rates & IFSC Incentives

Section 115BAA / IFSC Amendments

Key Update

- Units in International Financial Services Centre (IFSC) will now be taxed at 15% after tax-holiday period (earlier 22% or 30%)

- Effective from AY 2026-27

11. Dividend & Mutual Fund Expense Deduction Removed

Section 57

- Interest deduction no longer allowed against dividend/mutual fund income from AY 2026-27

- Prevents excessive tax sheltering

12. Stay of Demand Reduced

Section 220(6)

- Stay allowed by paying 10% tax (earlier 20%)

Need expert help with Personal Income Tax Filing, Tax Planning, Capital Gains Advisory, Corporate Tax Planning, Tax Audit, MAT Strategy or or Litigation Support?

Contact us today for ITR Filing, Refund Optimization, Corporate Tax Advisory, Litigation Support, Compliance Review & Strategic Tax Planning

We assist Salaried Individuals, NRIs, Business Owners, High-Net-Worth Taxpayers, MSMEs, Startups, Large Corporates & IFSC entities