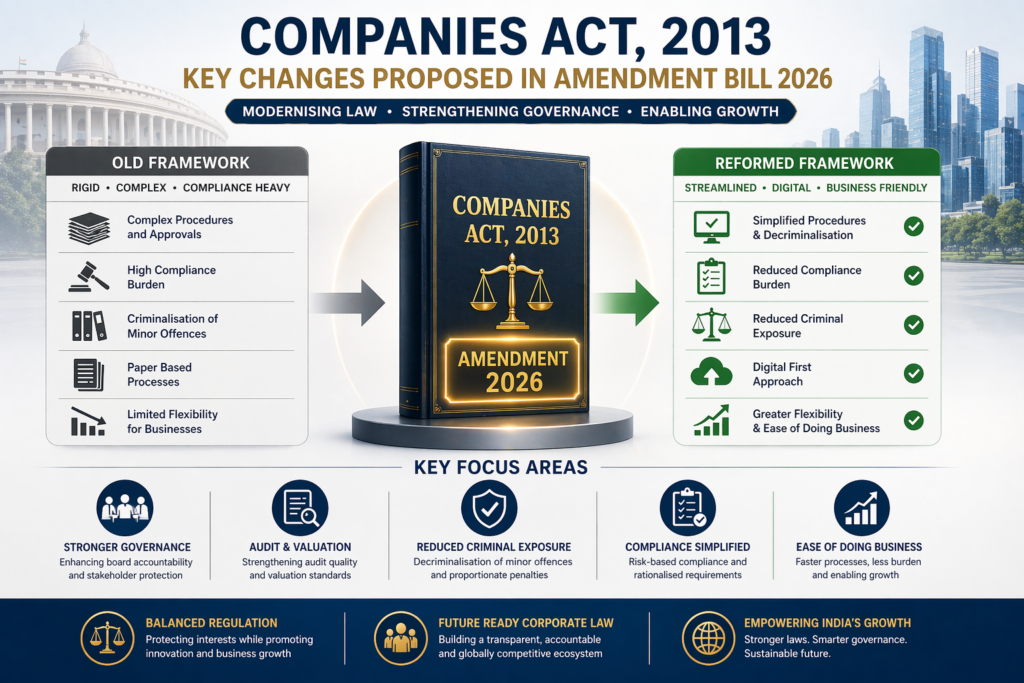

Companies Act, 2013: Key Changes Proposed in Amendment Bill 2026

The Corporate Laws (Amendment) Bill, 2026 proposes wide-ranging reforms to the Companies Act, 2013, aiming to modernise corporate regulation, reduce criminal exposure, and strengthen governance standards.

This amendment reflects a clear policy shift towards ease of doing business combined with stricter regulatory oversight in critical areas like audit, valuation, and corporate governance.

1. Expansion of Small Company Thresholds

The Bill proposes a significant increase in thresholds:

- Paid-up capital: ₹10 crore → ₹20 crore

- Turnover: ₹100 crore → ₹200 crore

Practical Impact:

This change will bring a larger number of companies under the “small company” category, allowing them to avail:

- Lesser penalties

- Reduced compliance burden

- Simplified reporting requirements

This is particularly beneficial for growing startups transitioning into mid-sized enterprises.

2. Financial Year Alignment Flexibility

The Central Government is empowered to allow companies to align their financial year ending to 31st March, based on business or commercial requirements.

Practical Impact:

- Useful for subsidiaries of foreign companies

- Simplifies group consolidation and reporting

3. Strengthening Incorporation Compliance & Digital Identity

A stricter compliance framework is introduced at the incorporation stage:

- Mandatory declarations by directors/KMP

- Mandatory certification by professionals (CA/CS/CMA/Advocate)

- Introduction of Section 12A requiring:

- Website

- Digital communication details

Practical Impact:

- Increased accountability of professionals

- Greater transparency and traceability of companies

4. IFSC Companies – A New Global Framework (Section 43A)

A major structural reform is introduced for companies operating in International Financial Services Centres (IFSC):

- Share capital must be maintained in permitted foreign currency

- Books of account to be maintained in foreign currency

- Existing companies must convert INR capital into foreign currency

Practical Impact:

- Boost to GIFT City and cross-border financial operations

- Alignment with global financial standards

5. Buy-Back Liberalisation (Section 68)

The Bill introduces flexibility in share buy-backs:

- Up to two buy-backs in a year

- Minimum 6-month gap between offers

- Removal of affidavit requirement

- Differential penalties for listed and unlisted companies

Practical Impact:

- Better capital management

- Increased flexibility for investor returns

6. NFRA Strengthening – A Major Regulatory Shift

The powers of the National Financial Reporting Authority (NFRA) are significantly expanded:

- NFRA becomes a body corporate

- Jurisdiction extended to all bodies corporate

- Power to:

- Issue directions

- Conduct investigations

- Impose penalties

- Enforce Compliance

New provisions (Sections 132A–132K) include:

- Auditor reporting obligations

- NFRA Fund

- Recovery of penalties

- Regulatory framework for audits

Practical Impact:

- Stronger audit oversight

- Increased accountability of auditors and audit firms

- Higher compliance expectations

7. CSR Framework Rationalisation (Section 135)

Key changes include:

- CSR applicability threshold increased to ₹10 crore

- Time for transfer of unspent CSR extended: 30 → 90 days

- Penalty increased up to ₹1 crore

- Exemptions for certain classes of companies

Practical Impact:

- Reduced burden on smaller companies

- Stricter compliance for large corporates

8. Auditor Regulation & Accountability

Amendments to Sections 139, 141, 144, 147, 148 introduce:

- Mandatory registration of audit partners

- Restriction on non-audit services (even post tenure)

- Exemption of certain companies from audit requirement

- Replacement of criminal penalties with civil penalties

Practical Impact:

- Improved audit quality

- Reduced criminal exposure

- Stronger professional discipline

9. Independent Directors (Section 149)

Key clarifications:

- Relaxation for professionals associated with firms (if transactions <10%)

- Inclusion of additional director tenure in total tenure

Practical Impact:

- Practical flexibility in appointing independent directors

10. DIN Governance (Section 154)

New provisions include:

- Mandatory periodic verification of DIN

- Power to deactivate/cancel DIN

Practical Impact:

- Stronger governance and accountability of directors

11. Director Disqualification (Section 164)

Key additions:

- “Fit and proper person” criteria

- Disqualification for professionals associated with company

- Reduction of disqualification period from 3 years to 2 years

Practical Impact:

- Strengthened corporate governance

12. Meetings Modernisation

(Sections 96, 100, 101, 173)

- AGMs/EGMs can be held:

Physically

Virtually

Hybrid mode

- Mandatory physical AGM once in 3 years

- Reduced notice period for VC meetings

Practical Impact:

- Digital governance becomes mainstream

13. Corporate Restructuring Reforms

(Sections 230–233, 233A)

- Approval threshold reduced to 75%

- Jurisdiction clarity

- Regulation of treasury/own shares

Practical Impact:

- Easier mergers and restructuring

14. Registered Valuers Reform (Section 247)

- Insolvency and Bankruptcy Board of India designated as Valuation Authority

- Mandatory registration & compliance framework

- Power to impose penalties

Practical Impact:

- Standardised and regulated valuation ecosystem

15. Strike-Off Provisions Strengthened (Section 248)

Companies may be struck off for:

- No significant transactions

- Non-filing for 2+1 years

Practical Impact:

- Removal of inactive/shell companies

16. New Recovery & Settlement Mechanism

(New Sections 454B–454D)

- Recovery Officer empowered for penalty recovery

- Introduction of settlement mechanism

- Mandatory 10% pre-deposit for appeals

Practical Impact:

- Faster enforcement and dispute resolution

17. Decriminalisation of Offences

Across multiple sections:

- Removal of imprisonment

- Introduction of civil penalties

Practical Impact:

- Shift from “prosecution” to “penalty-based compliance”

If you are a:

- Company Director

- Startup Founder

- CFO / Finance Head

The Companies Act, 2013 amendment will directly impact your compliance strategy, audit exposure, and corporate structuring.

- Impact analysis on your company

- Compliance restructuring

- Advisory on mergers, buy-backs & governance