Executive Overview

This notification provides a limited-time duty relief window:

- Effective Period: 1st April 2026 to 31st March 2027

- Applicable To: SEZ units manufacturing goods and clearing them to DTA

- Key Benefit:

- Capping of Basic Customs Duty (BCD)

- Conditional relief on AIDC (Agriculture Infrastructure and Development Cess)

This is not a blanket exemption—it is a conditional and compliance-heavy benefit.

Eligibility Criteria – Who Can Benefit?

To avail of this exemption, SEZ units must satisfy all four conditions:

- Manufacturing within SEZ

Goods must be manufactured in SEZ, not merely traded or re-exported.

- Production Timeline Condition

The unit must have commenced production on or before 31st March 2025.

- Exclusion of FTWZ Units

Units in Free Trade and Warehousing Zones (FTWZ) are not eligible.

- No “As Such” Clearance

Goods imported into SEZ and cleared without manufacturing do not qualify.

Core Conditions – The Real Gatekeepers

Even if eligible, the benefit is subject to three critical conditions:

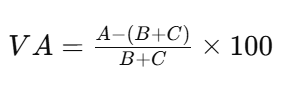

- Minimum 20% Value Addition

- Value addition must be at least 20%

- As per the prescribed formula:

A = Assessable Value of Final Product

- This is the total value of goods cleared to DTA

- Generally, it is the transaction value (selling price) of the finished goods

- Includes:

- Cost of production

- Profit margin

- All expenses forming part of value

In simple terms: Final sale value of manufactured goods

_________________________________________________________

B = Value of Imported Inputs

- Cost of raw materials/components imported from outside India

- Includes:

- CIF value (Cost + Insurance + Freight)

- Customs duties paid on such imports

In simple terms: Foreign inputs used in production

_________________________________________________________

C = Value of Domestic Inputs

- Cost of inputs procured from within India (DTA)

- Includes:

- Raw materials

- Consumables

- Components purchased locally

In simple terms: Indian inputs used in production

- 30% Cap on DTA Clearance

- DTA sales cannot exceed 30% of the highest FOB export value in the last 3 financial years

- No Double Benefits

- No duty drawback or export incentives can be claimed on inputs

What Qualifies as “Manufacture”?

The notification adopts a strict definition of manufacture, requiring:

do NOT qualify, which could impact industries like electronics and pharma.

Compliance Requirements

To claim the exemption, SEZ units must follow strict procedural steps:

- File Bill of Entry for home consumption

- Obtain certificate from Development Commissioner confirming:

- Production start date

- Export performance

- Value addition

- Submit undertaking for duty liability in case of non-compliance

- Be ready for audit under SEZ Rules, 2006

Expert Insight

Businesses should not rush blindly to claim this benefit.

A proper evaluation of:

- Value addition calculation

- Export history

- Product classification

- Compliance capability

is essential before availing the exemption.

The window is limited. The risks are real. The opportunity is strategic.